The Office of Tax Simplification (OTS) has published its second report on Inheritance Tax. The report comes after the Chancellor requested a review of administrative and technical aspects of the tax back in January 2018. The first report was released in November 2018 and covered the administration of Inheritance Tax. This second report now explores the key complexities and technical issues that arise from the way the tax works.

The OTS followed a consultation process which included an online survey that received almost 3,000 responses, and a call for evidence which saw 500 email and 100 written responses. Additionally, the OTS received contributions from representative bodies, professional advisers and academics, among others. They also consulted with a wide range of organisations, including Kings Court Trust. With the astounding levels of interest shown about the review, the OTS has highlighted how the tax is unpopular and often misunderstood among members of the public.

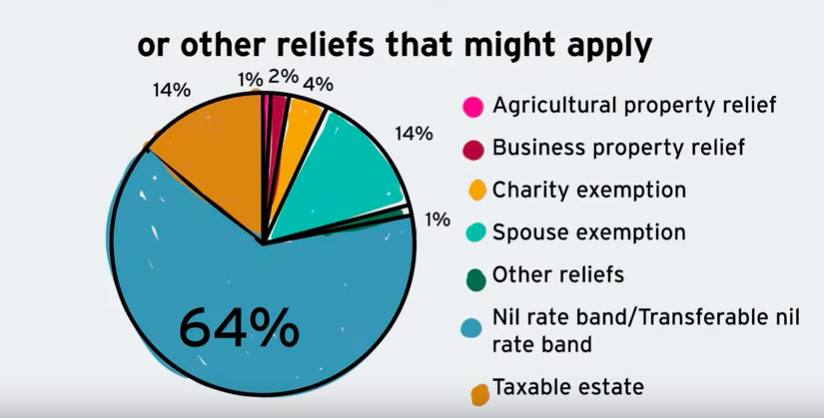

The video below has been created by the OTS to provide a high-level summary of what the Inheritance Tax report is about:

The OTS has highlighted that fewer than 5% of all deaths (25,000 estates) are subject to Inheritance Tax each year. However, around 275,000 Inheritance Tax forms are still completed. OTS Chairman, Kathryn Cearns OBE said:

“Although only a small number of people pay Inheritance Tax each year, a far greater number worry about it. The OTS’s packages of recommendations would go some way to achieving the goal of making the tax easier to understand and simpler to comply with.”

In this second report, the OTS makes 11 recommendations which aim to make the structure of Inheritance Tax clearer and easier to understand. The recommendations are focused on three main areas which include lifetime gifts, interaction with Capital Gains Tax, and business and farms. Some of the key recommendations made by the report include:

1. Lifetime gifts

From consultations, the OTS found that the way in which the tax works in relation to gifts is complex, confusing and can require extensive record keeping. Therefore, they’ve suggested:

- Introducing an overall personal gifts allowance to replace the various lifetime gift exemptions. They suggest setting the allowance to a sensible level and incorporating a small gifts allowance. Additionally, they advise that the government should either reform the exemption for normal expenditure out of income or replace it for a higher personal gift allowance.

- Reducing the period during which a lifetime gift may be subject to Inheritance Tax to five years instead of the current seven-year period.

- Abolishing taper relief which is the rate of Inheritance Tax on gifts made more than three years before the date of death.

- The 14-year rule means that gifts made outside of the seven-year period need to be accounted for when calculating the Inheritance Tax due. The OTS recommends removing the need to account for gifts made outside of the seven-year period.

- Exploring options to simplify and clarify the rules on who is liable to pay tax on lifetime gifts and the allocation of the Nil Rate Band.

2. Capital Gains Tax

The report highlights how

“the interaction between Inheritance Tax and Capital Gains Tax is complex and can distort decision making.”

Typically, there is no Capital Gains Tax on death and the report implies that this stops people from passing assets to the next generation in their lifetime. Therefore, the OTS recommends that Capital Gains Tax should be changed as a result.

3. Businesses and farms

Businesses and farms are often not subject to Inheritance Tax as they may receive relief from the business property relief (BPR) or agricultural property relief (APR). The requirements to qualify for BPR are different from the conditions for Capital Gains Tax business reliefs. As a result, the OTS has identified that if the tests were standardised, it could be easier for business owners to decide whether to pass on their business during their lifetime or upon their death.

4. Life assurance and pensions

Currently, if a term insurance policy is written in Trust, it can make a huge difference to its Inheritance Tax status. Consequently, the OTS has advised the government to consider making death benefit payments from term life insurance Inheritance Tax free, removing the need for them to be written in Trust.

The OTS provides independent advice on how to simplify the UK’s tax system, to make improvements for taxpayers. It’s now down to the government and parliament to decide whether they wish to implement the changes. If you want to find out more about the recommendations, the full report released by the OTS can be found here.

Source: Kings Court Trust

At Sussex Will Writers, we frequently find that people are confused by the legal and tax affairs associated with administering a deceased person’s estate. Therefore, we hope that any changes that are made to the Inheritance Tax structure effectively simplifies the tax and makes it easier for families to understand.

Sussex Will Writers help to take care of the complicated practicalities after death, so you can focus on life’s important moments. If you have any questions about estate administration or Inheritance Tax, call us on 01903 533681 or get in touch by emailing: info@sussexwillwriters.co.uk

![]() Sussex Will Writers

Sussex Will Writers

T: 01903 533681

M: 07734 744886

E: info@sussexwillwriters.co.uk